In the Long Run Long-Term Government Bonds Are Safe, But We Are a Long Time Dead

Earlier in

the year the Swiss National Bank, Switzerland’s central bank, released its

latest report. While reading the news covering the bank’s financial results, I

was surprised twice.

First, it

turned out that Switzerland’s central bank still has its stock trading on

the SIX Swiss stock exchange. Now that’s what I call Die-Hard Capitalism!

Second, I was

surprised by the reaction of many observers to the financial results reported

by the SNB. They were virtually shocked that it reported the largest loss – 132

Swiss francs (143 billion US dollars) – in its 115-year history (see Reference

1 below). Switzerland has accumulated foreign exchange reserves to the tune of

more than 1 trillion US dollars invested in foreign currencies, gold, stocks, and,

of course, various government bonds. Therefore, the fact that the bank reported

stock- and foreign exchange-related losses does not surprise anyone. However, people

are often shocked when faced with large losses resulting from investments in

“safe” government bonds.

Just ask any

pension fund or insurance company in any developed country whether

government bonds deserved their “safe-haven” status in 2022 in the context

of the most serious geopolitical crisis in the last 30 years, dramatic supply

chain disruptions, and the highest inflation rates in the last 40-50 years.

The

government bond topic is rapidly becoming politically sensitive when you see newspaper

headlines such as these: “A million older workers face new pensions

misery: Bond rout wipes a third off funds – just as retirement looms. The

retirement plans of up to a million workers lie in tatters as the recent

collapse in supposedly safe government bonds battered the value of their

pension pots.” (see Reference 2 below).

Despite the

fact that the bond market is larger than the stock market, the vast majority of

non-professionals and many professionals (!) have only a very vague

understanding of bonds and interest rates. Therefore, it would be reasonable to

recall the basics of financial theory and history.

The theory of

finance says that the purchase of bonds provides their owner with the

opportunity to become the creditor of a company, an international

institution, or a government. In other words, bonds are loans traded in the

financial markets.

The

fundamental theory of finance also says that the cost of any financial

instrument depends on the amount of cash flow you can expect to receive from

investing in it. What is the cash flow an investor can expect to receive

when he or she purchases a bond? We have already mentioned that bonds are, in

fact, market-traded loans issued to governments or companies. That is why, when

purchasing a bond, an investor can expect to receive usually fixed periodic

payments (bond coupons), as well as the principal or face amount of this bond

when it is redeemed.

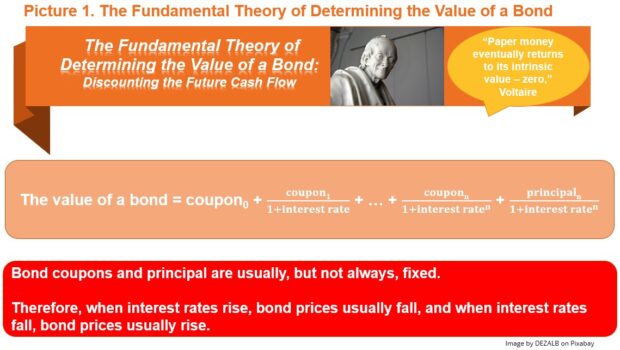

Still, the

simple addition of a sequence of cash flows from different time periods is not

appropriate since “Paper money eventually returns to its intrinsic

value – zero,” as the famous French philosopher Voltaire put it. That

is why the fundamental theory of finance also asserts that the cash flows

received in the future have less real purchasing power compared to the cash

flows received today. Scientifically speaking, the value of a financial

investment depends on the discounted cash flow that the investor can expect to

receive when making this investment (see picture 1 below).

Discounting,

or value reduction, occurs by using interest rates. Interest

rates consist of three components: first, a risk-free interest rate that

reflects the time effect between consumption today and consumption in the

future. It is usually paid by the governments of the most reliable borrowing

countries; second, a market-risk premium paid by all private companies since

they carry a higher risk of not meeting their obligations when compared to

governments; third, a specific-risk premium paid by each specific company.

Since both

the amount of bond coupon payments and its principal amount, when the bond is

redeemed, are usually fixed, it can be concluded that changes in its price are

almost entirely explained by changes in the interest rate used to discount the

bond’s expected cash flows. However, these changes may occur for various

reasons. The changes may occur because there is an increase in the risk-free

interest rate delivered by the central bank fighting high inflation. There

might also be a rise in the market-risk premium due to some economic or

political upheavals, for example. Or there might be a rise in the specific-risk

premium for a particular company due to any negative events directly related to

it. Still, the general conclusion is straightforward: when interest rates

rise, bond prices usually fall, and when interest rates fall, bond prices

usually rise.

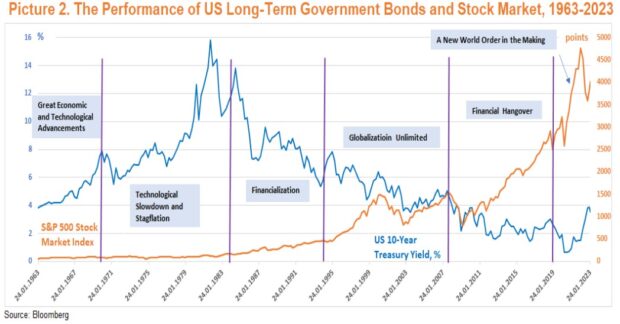

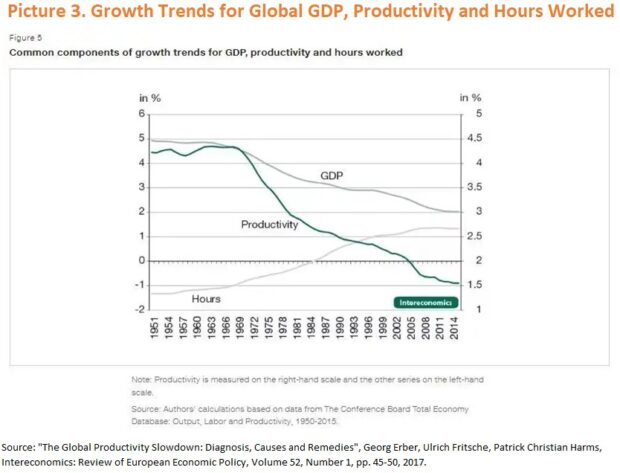

Economic

history strongly suggests that that the most important variable in the world

of finance is the PRICE OF LONG-TERM MONEY, that is long-term interest

rates. It also says that the most important variable in the world of real

economy is LABOR PRODUCTIVITY. Did you know that the growth rate of real

wages is determined by the growth rate of labor productivity? Now you can see

why the growth rate of real wages has been so slow for decades (see Picture 2

and Picture 3 below).

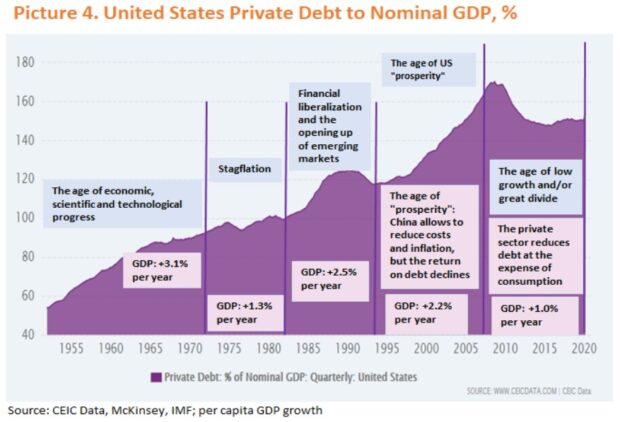

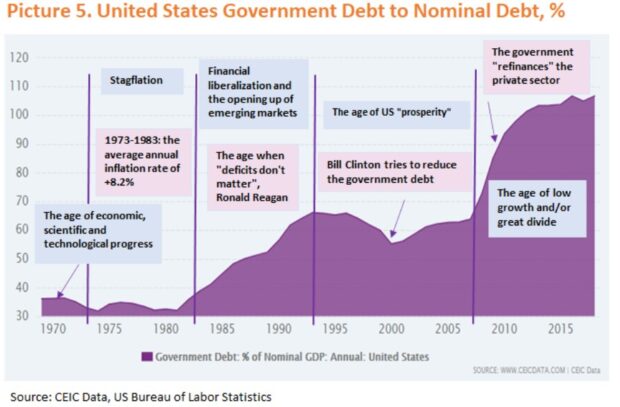

If we are not

sufficiently productive, then various types of financial engineering — both monetary

and fiscal — will only help us buy some time before we are forced to curb our

consumption (see Picture 4 and Picture 5 below).

Now we can

present the shortest possible course of economic and financial history of

the last 60 years:

Stage 1. From

the late 1960s to the early 1980s. Technological Slowdown and Stagflation. The

growth rate of technological progress and labor productivity started slowing

down. This led to a slowdown in the growth rate of real GDP. A loose monetary

and fiscal policy aimed at supporting the faltering economy fueled demand-pull

inflation. The gold standard was abolished. Now fiat (“paper”) money was no

longer pegged to gold. This spurred inflation even further. Negative supply

shocks (two oil crises) paved the way for shortages and cost-push inflation (“stagflation”).

Inflation was soaring, long-term interest rates were soaring, stock prices were

languishing.

Stage 2. From

the early 1980s to the early 1990s. Financialization.

The US central bank started implementing a shock therapy strategy by hiking

interest rates sharply, thereby slowing down inflation, and inevitably causing

a deep recession in the economy. To support the economy and consumption a loose

fiscal policy was initiated. Most importantly, the financial sector was

liberalized to make it easier for companies and private individuals to borrow

money. The growth rate of real GDP started to accelerate. Long-term interest rates

were falling sharply, while stock prices were rising. The growth rate of labor

productivity was still slowing down.

Stage 3. From

the mid-1990s to the mid-2000s. Globalization Unlimited. A

positive supply shock following the opening-up of China, the former Soviet

bloc, and other emerging markets. New supply chains, the outsourcing of

manufacturing facilities to poorer countries, and the global migration of labor

reduced costs and eliminated the threat of cost-push inflation. This allowed to

lower interest rates even further, thus encouraging private individuals to

borrow more to support consumption. Finally, demand-pull inflation started to

reappear. Stock and other asset prices were rallying due to rising profits,

since the demand-pull inflation for final products was far above the cost of

resources, labor, and borrowed money. The growth rate of labor productivity was

still slowing down.

Stage 4. From

the late 2000s to the late 2010s. Financial Hangover. The

declining marginal economic effect from additional private debt reached its

tipping point: more private debt could not support more consumption and higher

asset prices anymore. Asset prices started to collapse, thus undermining the

creditworthiness of private borrowers and their lenders. The governments

started to refinance the private sector through stimulus programs, while the

central banks started to refinance the governments by buying public debt and

lowering long-term interest rates to zero and below. The private sector

stabilized its debt situation but at the expense of lower consumption.

Inflation was subdued. The growth rate of real GDP was meagre. Stock prices

recovered and resumed their meteoric rise since, first, input prices

(resources, labor, and interest rates) were falling; second, the amount of available

liquidity was substantially exceeding that of investable opportunities.

Cryptos, fintech and other alternative assets were thriving for the same

reason. The growth rate of labor productivity was becoming negative in some

countries.

Stage 5. From

the late 2010s to now. A New World Order in the Making. A

protracted period of low economic growth was undermining political stability

around the world. Geopolitical and domestic tensions were visibly on the rise.

Cracks began to appear in global supply chains due to trade wars, the pandemic,

and military conflicts. This led to the resurgence of cost-push inflation (“stagflation

revisited”). The central banks started raising interest rates, while asset and

stock prices are falling significantly. It is quite probable that the growth

rate of labor productivity has become negative in most countries.

Now you

probably understand that the era of financialization required low interest

rates. Furthermore, the era of financial hangover required even lower rates. As

a result, long-term interest rates were steadily declining leading to a

legendary Great Bond Bull Run of the last 40 years.

However,

there is no such thing as miracles, particularly, in finance. That is why these

developments also meant that the likelihood of a sharp rise in inflation and

interest rates at some point in the future was extremely high too. The two

remaining uncertainties were the timing and magnitude of this almost inevitable

rise. As we now know from economic theory, a rise in interest rates implies

a fall in bond prices. Furthermore, the longer the maturity of a bond is, the

more it is exposed to a rise of long-term interest rates.

Thus, before

investing in long-term government bonds, remember the following:

1.

In

terms of credit risk long-term government bonds are safe if they are

issued in the national currency of an issuing country.

2.

Since long-term government bonds may

have maturities of 10, 30, 50 or even 100 years, in terms of interest rate

risk, currency risk, liquidity risk, and inflation risk, they may be as risky

as other assets (!).

3.

In terms of interest rate risk

long-term government bonds are safe only if their periodic coupon payments are

floating. This means that the floating coupons are periodically adjusted to

reflect changes in short-term interest rates. In most cases, however, periodic

coupon payments are fixed. Therefore, a rise in long-term interest rates has a negative

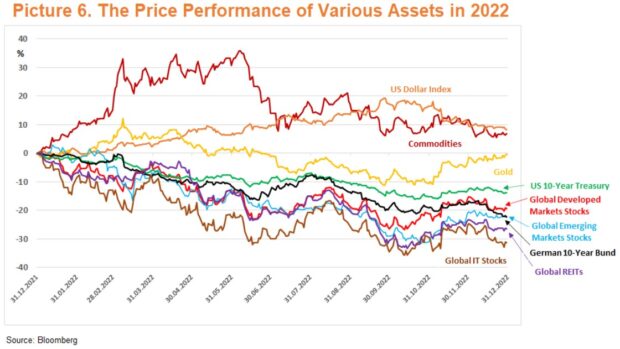

impact on the price of such fixed-rate bonds. That is why in 2022 the prices

of long-term government bonds issued by developed countries fell sharply in

unison with stock prices (see Picture 6 below).

4.

In terms of currency risk if

you purchase a government bond denominated in a foreign currency for the

issuing country, then its credit risk is higher than the credit risk of an identical

bond denominated in the national currency of that country. Currency risk

also arises if you purchase a government bond denominated in a currency other

than your base currency. For example, US investors who held unhedged euro-denominated

German government bonds during 2022 suffered losses not only resulting from a

fall in bond prices, but also from a fall in the euro exchange rate versus the

US dollar. At the same time, Turkish investors gained from a rise in the euro

exchange rate against the Turkish lira (see Picture 7 below).

5.

In terms of liquidity risk illiquid

issues of government bonds may have a price disadvantage compared with identical

liquid issues. For example, investors may demand an illiquidity premium for

government bond issues that are small in terms of size. If you need to sell

such a paper urgently, you may find out that its bid price is reduced by the

amount of this illiquidity premium.

6.

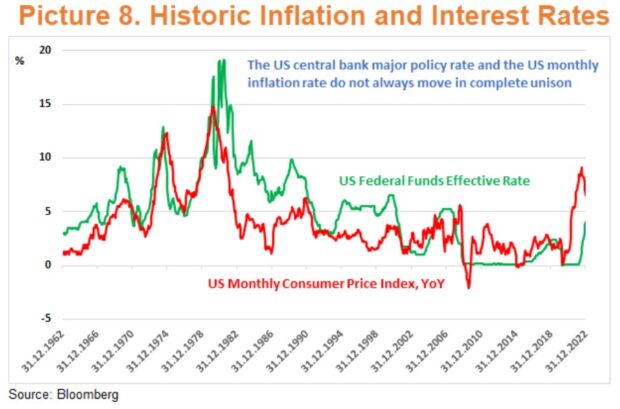

In terms of inflation risk

even floating-rate government bonds do not guarantee that their prices will adjust

to fully reflect changes in the rate of inflation (see Picture 8 below). For

example, the monthly inflation rate in the United States in 2022 peaked at 9.1%,

while the 6-month US dollar LIBOR did not exceed 5.25%. In the eurozone the monthly

inflation rate peaked at 10.6% in 2022, while the 6-month EURIBOR interest rate

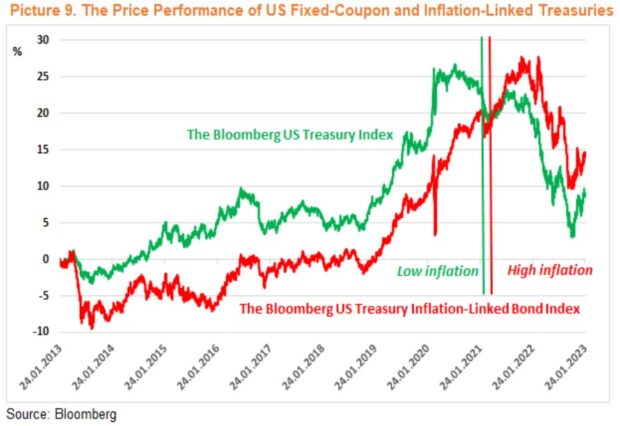

did not exceed 2.8%. Investing in government inflation-linked bonds whose

coupons are regularly adjusted to reflect changes in the rate of inflation may

help you hedge against consumer price rises to a greater degree. Though in a

low inflation environment they may demonstrate a significant price underperformance

too (see Picture 9 below).

John Maynard

Keynes, one of the most famous economists of the 20th century, as

well as a successful investor and speculator, once said that “in the long

run we are all dead.” To paraphrase him slightly, I would say that when

investing in bonds remember that in the long run long-term government bonds are

safe, but we are a long time dead.

References:

1.

“SNB $143 Billion Record Loss Costs

Swiss Usual Payout”, Bastian Benrath, Bloomberg, 9 January 2023.

2.

“A Million Older Workers Face New Pensions

Misery: Bond Rout Wipes a Third Off Funds – Just as Retirement Looms”, Patrick

Tooher, This Is Money.co.uk, 31 December 2022.